What is the term of a mortgage?

What is the term of a mortgage in Switzerland?

In Switzerland, the term of a mortgage corresponds to the period during which the conditions of your contract (in particular the interest rate and certain clauses) are fixed. Depending on the type of mortgage, this term can range from a few years (2–3 years) up to 10, 15 or even 20 years for certain fixed-rate mortgages. We then speak of the mortgage term or, more concretely, the term of your mortgage loan.

The key point to remember: the mortgage term is not the same thing as the total period during which you will remain an owner with bank financing. You can renew, adjust or change products at each contract maturity.

Understanding the term of a mortgage in Switzerland

Mortgage term by product type

The term of your mortgage depends heavily on the type of loan you choose:

- Mortgage with a fixed rate

You choose a contractual term (for example 5, 10 or 15 years) during which:- the interest rate remains the same,

- your monthly payments (or quarterly/half-yearly interest) are predictable,

- an early exit is generally penalized (termination fee).

- SARON mortgage (market variable rate)

The interest rate is linked to SARON, which fluctuates depending on the money market. The term of a mortgage loan of the SARON type does not correspond to locking the rate, but rather:- to the minimum period during which you remain in this product (often 3 years, 5 years, etc.),

- with the option to adjust your strategy at each maturity, while remaining exposed to rate fluctuations.

- Mixed or split mortgages (mixed rate)

You can split your financing into several tranches with different mortgage terms, for example:- 1/3 over 5 years,

- 1/3 over 8 years,

- 1/3 over 10 years.

This makes it possible to stagger renewal risks over time.

Typical examples of terms

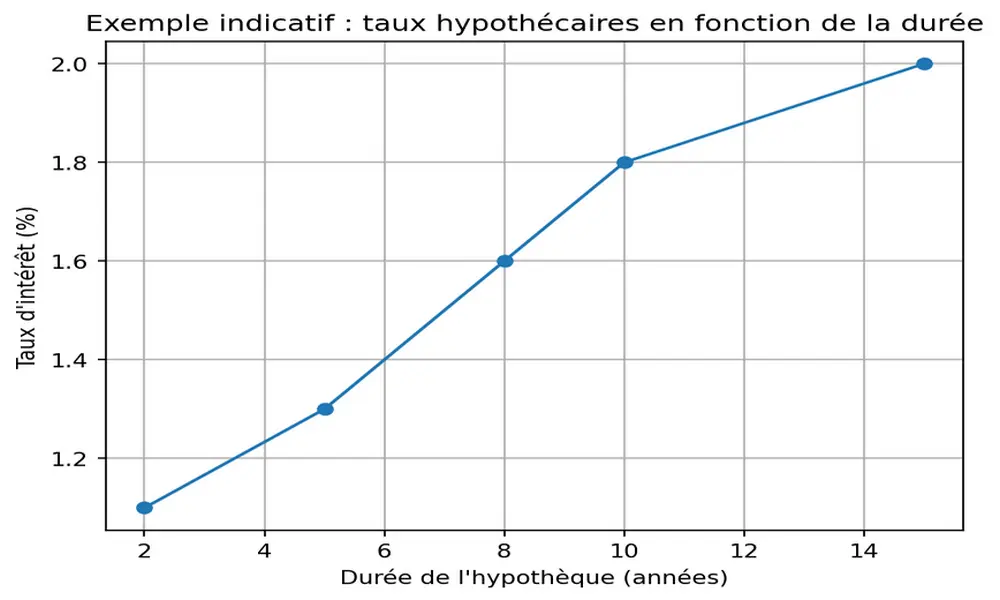

In practice, the following terms are often used for a fixed-rate mortgage:

- short term: 2 to 4 years,

- medium term: 5 to 7 years,

- long term: 10 to 15 years (or more depending on certain institutions).

For most homeowners, the term of your mortgage is chosen based on:

- your investment horizon (keep the property, sell, move),

- your risk tolerance,

- your monthly budget,

- and your view on how rates may evolve in the future.

Mortgage term and its impact on the interest rate

The longer the term, the higher the rate is (in general)

Generally speaking, the longer the term of a mortgage loan is, the longer the bank commits, and the more:

- you gain budget stability (rate locked for longer),

- but you pay a term premium in the form of a higher rate.

Conversely, a shorter term is often associated with:

- a lower interest rate at the outset,

- but greater uncertainty about what will happen at maturity (renewal in a potentially higher-rate environment).

This can be summarized as follows:

- Short term

→ Lower initial rate, but risk of rate increases at renewal. - Long term

→ Higher initial rate, but strong visibility on your budget for many years.

Numerical example: 5 years vs 10 years

Let’s imagine a mortgage of CHF 800 000 on your primary residence, amortized indirectly (interest only over the period considered):

- Option A: 5-year fixed-rate mortgage at 1.40%

- Option B: 10-year fixed-rate mortgage at 1.80%

Over the first 5-year period:

- Interest with Option A:

800 000 × 1,40 % = CHF 11 200 per year, i.e. CHF 56 000 over 5 years. - Interest with Option B:

800 000 × 1,80 % = CHF 14 400 per year, i.e. CHF 72 000 over 5 years.

You therefore pay CHF 16 000 more over 5 years with the longer term. In return:

- With Option A (5 years), you will have to renew your mortgage after 5 years, without knowing future rates in advance.

- With Option B (10 years), the term of your mortgage protects you for 10 years against a rise in rates.

If, at renewal after 5 years, rates have risen sharply (for example to 2.50% or 3.00%), the decision to choose a longer term could prove worthwhile over the overall period. Conversely, if rates stay low or fall, you will have paid a safety premium. Run a simulation with our mortgage calculator.

How to choose the term of your mortgage?

The right questions to ask yourself

To choose the term of your mortgage loan, it is useful to ask yourself the following questions:

- How long do you think you will keep this property?

- If you plan to sell, move or separate from the property within 3 to 5 years, a very long term (15 years) may be less suitable, because an early exit could lead to penalties.

- What is your tolerance for interest-rate risk?

- If an increase of 1 or 2 percentage points on your monthly payment would endanger your budget, a longer and more stable term may be appropriate.

- Is your financial situation likely to change?

- Rapidly growing income, possible inheritance, accelerated amortization… These factors can influence the optimal mortgage term.

- Do you want a simple strategy or a more sophisticated one?

- A single term (for example 10-year fixed) is simple to manage.

- Several tranches with different terms make it possible to optimize the risk profile, but are more complex to monitor.

Typical profiles for the term of a mortgage loan

Without being hard rules, here are a few common profiles:

- Young couple buying their first primary residence

- Tight budget, need for visibility.

- Often a term of your mortgage of 7 to 10 years, or even 15 years on part of the mortgage, to secure the rate.

- Real estate investor

- Looks to optimize returns, with a higher tolerance for risk.

- May sometimes combine a SARON mortgage (flexible, but volatile) with one or two fixed tranches of different terms (5 years + 10 years, for example).

- Homeowner close to retirement

- Wants maximum stability on the cost of their mortgage loan.

- May favor a relatively long fixed term (10–15 years) or a mix of terms that helps avoid renewing everything at once.

Effect of the term on the total cost of the loan

Comparing several terms for the same amount

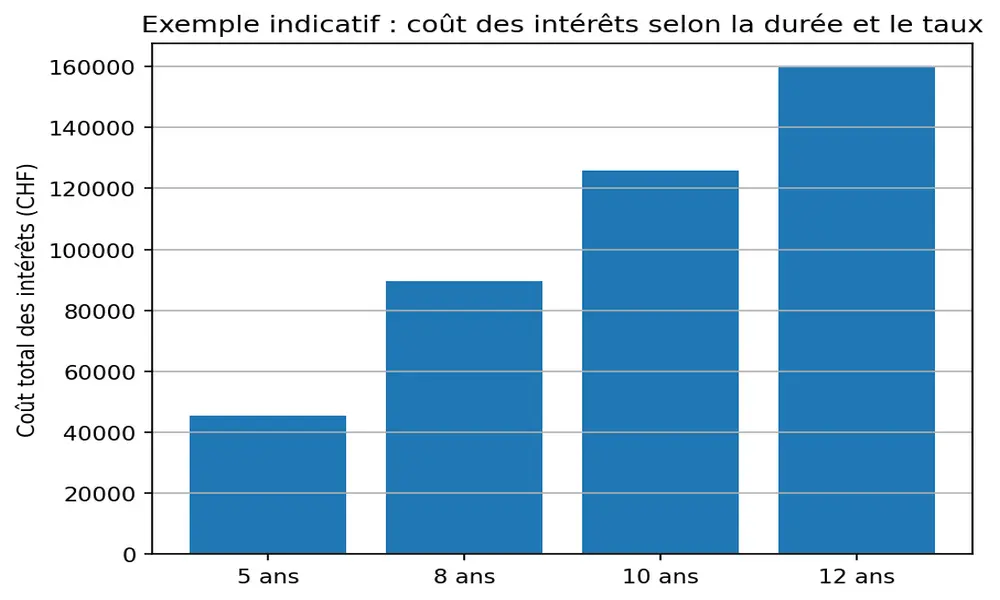

Let’s take an example with an amount of CHF 700 000 and three fixed-rate mortgage term assumptions:

- 5 years at 1,29 %

- 8 years at 1,61 %

- 10 years at 1.79%

- 12 years at 1,90 %

Interest (excluding amortization):

- 5 years at 1,29 %

→ 700 000 × 1,29 % = CHF 9 030 per year, i.e. CHF 45 150 over 5 years. - 8 years at 1,61 %

→ 700 000 × 1,61 % = CHF 11 270 per year, i.e. CHF 90 160 over 8 years. - 10 years at 1,79 %

→ 700 000 × 1,79 % = CHF 12 530 per year, i.e. CHF 125 300 over 10 years. - 12 years at 1,90 %

→ 700 000 × 1,90 % = CHF 13 300 per year, i.e. CHF 159 600 over 12 years.

We can see that the longer the term of a mortgage loan is, the higher the total interest paid, even if the monthly payment remains stable. The challenge is therefore to find the right compromise between:

- long-term security,

- and total interest cost.

Example of a combined strategy

For example, you could:

- Put CHF 400 000 on a 5-year term at 1,30 %,

- and CHF 300 000 on a 10-year term at 1,80 %.

In this way, part of your mortgage loan term remains short (and potentially cheaper), while another part is secured over a longer period. At each tranche maturity, you can adjust your strategy depending on the rate environment, your budget and your plans.

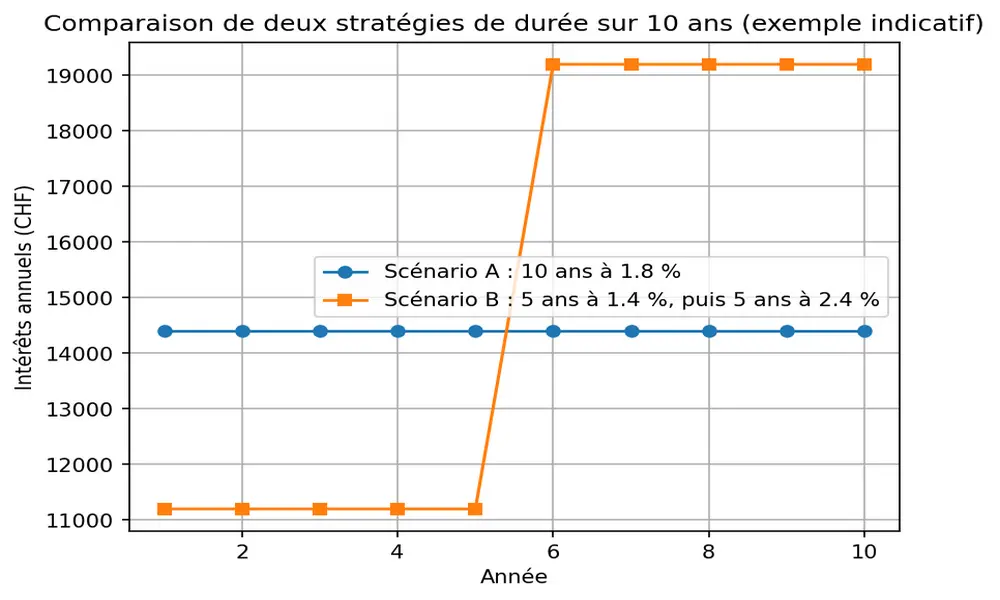

Below is an example of a CHF 800 000 loan:

- Scenario A: 10-year term with a 1.8% rate => CHF 14 400 of interest to pay per year

- Scenario B (renewal): 5-year term at 1.4% => CHF 11 200 of interest/year, then a 5-year renewal at a rate of 2.4% if rates rise => CHF 19 200 of interest/year