Buying vs renting: which option should you choose in Switzerland?

Buying or renting a property: what should you choose in Switzerland?

The right answer to « buy or rent » depends less on a belief (« property is always better ») than on your ownership time horizon, your life stability, your financial capacity (according to Swiss banking criteria) and your risk tolerance (rates, the property market, unexpected events). Put simply: renting gives you flexibility and better short-term predictability; buying allows you to build up capital over time, but comes with specific costs and risks (rates, works, resale).

A key point is often misunderstood: in a purchase financed with a mortgage, the part that is « comparable to rent » is not the property price, but mortgage interest. And that interest does not go « into an owner’s pocket »: it goes to the bank as remuneration for the loan. It is an expense that is “consumed”, just like rent… except that, in parallel, you own an asset (the home) whose value can evolve, generally upward.

- Understanding expenses: renting vs buying with a mortgage

- Buy or rent: a practical method to decide without getting it wrong

- Numerical examples (simply, without an “illusion of accuracy”)

- Renting vs buying: important points that are often overlooked

- How to decide “buying or renting in Switzerland” for your situation

Understanding expenses: renting vs buying with a mortgage

Renting: what you pay, and what you do not have to pay

When renting, your main expense is the rent (and sometimes certain charges). The logic is simple:

- you pay for the use of the home,

- you do not bear (or bear only a small part of) the risk of major works,

- you do not have to tie up 20% of equity as when buying a property,

- in the end, you have no asset linked to that home (no capital built up through this payment).

Buying: interest, charges, maintenance, and capital

When buying, your cash flow is generally split into two broad categories:

- What looks like “rent”

- mortgage interest : this is the “price of money” borrowed (so an expense that goes to the bank).

Even if you do not make any amortization, this interest exists as long as the mortgage exists.

- What is specific to being an owner

- ongoing maintenance, future renovations, condominium fees (PPE) if it is an apartment, building/liability insurance depending on the case, etc.

These items are often underestimated. A simple rule (to be refined depending on the property) is to set aside an annual budget (for example a percentage of the property value) for maintenance/non-recoverable charges.

- What creates (or destroys) value

- the property value can go up or down. This change is not an “expense”, but an evolution of your net worth.

This is exactly why the “rent vs interest” comparison is useful but insufficient: buying combines expense + investment.

Buy Rent: a practical method to decide without getting it wrong

1) Your time horizon (the most decisive factor)

The longer your horizon, the more buying can become relevant, because:

- acquisition costs (notary, land registry, possible duties, etc.) are “spread” over more years,

- the probability of benefiting from value growth (or at least stabilizing the cost of use) increases,

- you reduce the risk of having to sell “at the wrong time”.

Conversely, if you think you will stay 2–4 years, renting is often more rational (except in very specific cases).

2) Your life and income stability

The question “should you buy or rent” is also a question of mobility:

- change of employer or canton,

- possible separation, blended family,

- uncertainty about the size of home you need.

In Switzerland, selling can be quick in some areas, but it is not guaranteed, and a sale under time pressure reduces your negotiating power.

3) Your “Swiss-style” borrowing capacity

Banks apply theoretical affordability criteria (imputed rate, maintenance, amortization required in some cases). Even if, in real life, your rate is low, the bank’s assessment can limit your buying capacity. Result: you may be comfortable with your real budget, but blocked by financing approval.

4) Your risk tolerance (rates and market)

- If your mortgage is variable-rate or indexed (e.g., SARON), you accept potentially significant variability in interest.

- With a fixed rate, you gain visibility, but you sometimes pay a safety premium.

On the market side, real estate can stagnate or correct. Buying then becomes more of a “use + stability” choice than a “return” choice.

Numerical examples to compare buying vs renting

To illustrate the difference between buying and renting, here is a simple 10-year scenario:

Assumptions (example)

- Property: CHF 500’000

- Equity: 20% = CHF 100’000

- Mortgage: CHF 400’000

- Fixed rate : 2.0%

- Mortgage interest: CHF 8’000/year

- Owner maintenance/charges: 1.0%/year of the initial value (purchase price) = CHF 5’000/year

- Comparable rent: CHF 1’600/month = CHF 19’200/year

- Property value growth (capital appreciation): 2.0%/year (conservative assumption based on history)

Results after 10 years

- Total rent paid (renting): CHF 192’000

- Total “owner costs” paid (interest + estimated maintenance/charges): CHF 130’000

- Property value gain (2%/year over 10 years): CHF 80’000

- Capital at the end of the mortgage term linked to the property (initial equity + growth): CHF 180’000

Interpretation:

- On annual expenses, it may be that paying interest + maintenance costs less than rent (depending on the rent level, the rate, and actual maintenance).

- But buying ties up CHF 100’000 of equity from the start (capital immobilized).

- And the major difference: when buying, you have an asset value (the property) part of which can become cash if you sell.

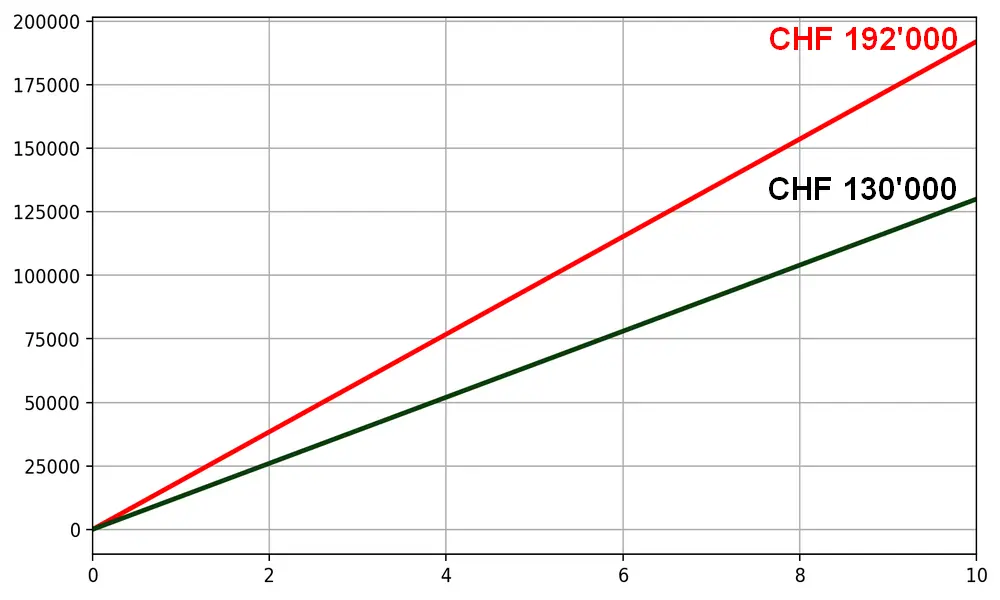

“Buy Rent” comparison over 10 years WITHOUT amortization

- X-axis: years (0 to 10)

- Y-axis: cumulative amounts paid (CHF)

- Red curve: cumulative rents CHF 19’200/year -> CHF 192’000 over 10 years

- Dark green curve: cumulative mortgage interest + charges

- interest: CHF 8’000/year (2% of CHF 400’000)

- charges: CHF 5’000/year (1% of CHF 500’000)

- total owner “spent”: CHF 13’000/year → CHF 130’000 over 10 years

- End point at 10 years:

- rents: CHF 192’000

- interest + charges: CHF 130’000

- share of the property value “that belongs to you”: CHF 180’000 = 100’000 initial equity + 80’000 capital gain

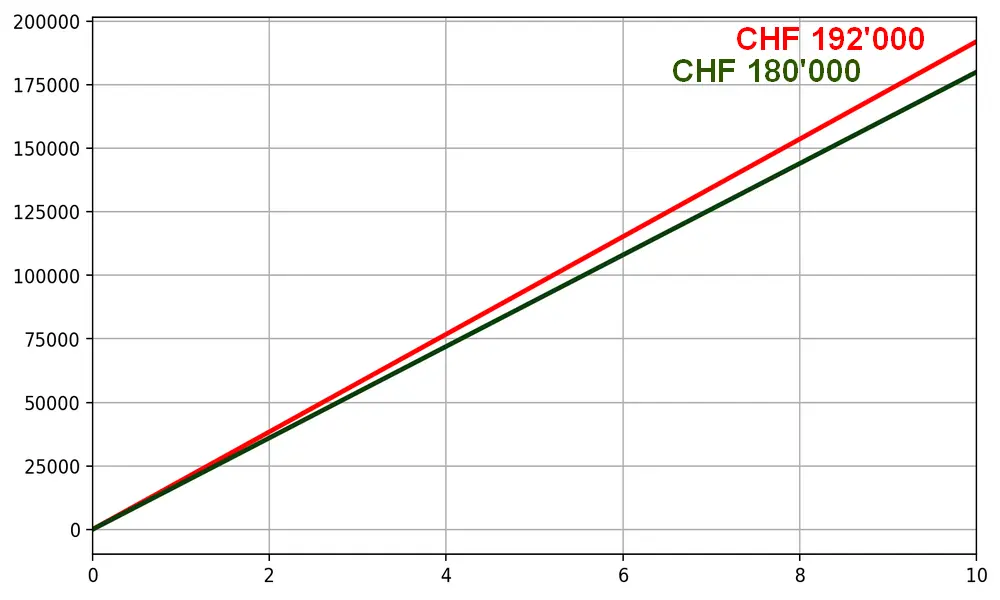

“Buy Rent” comparison over 10 years WITH amortization

- X-axis: years (0 to 10)

- Y-axis: cumulative amounts paid (CHF)

- Red curve: cumulative rents CHF 19’200/year -> CHF 192’000 over 10 years

- Dark green curve: cumulative interest + charges + amortization (total cash paid)

- interest: CHF 8’000/year

- charges: CHF 5’000/year

- amortization: CHF 5’000/year

- total cash paid: CHF 18’000/year → CHF 180’000 over 10 years

- End point at 10 years:

- rents: CHF 192’000

- total owner cash (interest + charges + amortization): CHF 180’000

- share of the property value “that belongs to you”: CHF 230’000 = 100’000 initial equity + 80’000 capital gain + 50’000 amortization

Renting vs buying: important points that are often overlooked

Taxes and deductions

In Switzerland, taxation can influence the balance (depending on canton and situation):

- the deduction of mortgage interest often possible (within certain limits),

- depending on the canton and the applicable rules, maintenance costs are sometimes deductible,

- depending on the rules in force, some systems include mechanisms similar to “imputed rental value” (to be considered in your calculation).

Practical conclusion: do not decide only on a “raw” Excel sheet; include a tax estimate if the stakes are significant.

Opportunity cost of equity

Renting sometimes allows you to invest part of your capital instead of tying it up in the home. This point often changes the conclusion when:

- your equity is high,

- you have an investor profile and accept volatility,

- the rental market is reasonable relative to purchase prices.

Works, PPE and unexpected costs

Buying can cost “more” than expected if:

- energy renovations,

- PPE charges increase,

- renovation fund is insufficient,

- hidden defects or structural works.

For a robust decision, build in buffers: this is not pessimism, it is risk management.

How to decide “buying or renting in Switzerland” for your situation

Use a 4-question logic:

- How long do you think you will stay in the property (realistic, not “ideal”)?

- Does your budget comfortably pass the bank’s theoretical affordability?

- Do you prefer flexibility (renting) or asset stability (buying)?

- Have you budgeted for maintenance and accepted that interest is a “consumed” cost that remunerates the bank?

If you are stable (7–10 years and more), with strong affordability and a coherent project, buying often becomes relevant. If you are in a transition phase, if your horizon is short, or if you want to minimize commitments, renting is often the most rational choice.