Mortgage rate trends in Switzerland: all you need to know

- A look back at the historical evolution of mortgage rates in Switzerland

- The impact of the mortgage interest rate on a home loan

- Why it’s important to plan your mortgage application ahead

- What are the current mortgage rates?

- What are the forecasts for rates until the end of the year?

- What factors influence mortgage rates?

- Fixed, variable or mixed mortgage: how to choose?

- Frequently asked questions about mortgage rates

Are you planning to buy a property, renegotiate your loan or simply understand the market better? Are you wondering whether rates will rise, fall or stabilise in the coming months? You’re in the right place!

Mortgage rate trends in Switzerland directly influence the cost of your loan and your purchasing power. These rates depend on many factors: SNB policy, inflation, economic conditions, market pressure…

Here’s a clear and complete overview of the history of Swiss rates, current trends and forecasts, and the concrete impact of these fluctuations on your mortgage.

A look back at the historical evolution of mortgage rates in Switzerland

Over the past 20 years, Swiss mortgage rates have shown a marked downward trend, especially after the 2008 financial crisis. This drop was driven by the Swiss National Bank’s (SNB) very accommodative monetary policy, with a key rate close to zero or even negative for several years.

Between 2010 and 2020, 10-year fixed rates were often between 1% and 2%, sometimes even dipping below 1%.

2022–2023 marked a turning point, with a gradual rise in mortgage rates due to the rebound in global inflation and rate hikes by major central banks.

The impact of the mortgage interest rate on a home loan

The interest rate directly affects the total cost of your mortgage loan. Even a small difference of 0.5% can amount to several thousand francs over the repayment period.

Monthly payments

The higher the rate, the higher your monthly payments. For example, for a CHF 800,000 loan over 10 years:

- At 1.5%, total interest will be around CHF 120,000

- At 2.5%, it will climb to over CHF 200,000

This differential impacts your monthly budget, but also your ability to invest or save for other projects.

Borrowing capacity

Lenders take the rate into account when calculating your debt capacity. A high rate can reduce the maximum amount you can borrow, or lengthen the loan term needed to stay within set limits.

Why it’s important to anticipate your mortgage application

In an unstable economic context, locking in a good rate at the right time can make all the difference. That’s why working with a broker who monitors markets daily and helps you choose the best strategy according to your goals is valuable.

Also, before signing your loan, compare several offers and simulate the impact of different rate scenarios. Signing too quickly without comparing can unnecessarily increase your financial burden. Our brokers support you at every step to make the right choice, at the right time, with full transparency.

By anticipating, you can prepare financially and have a better chance of securing a favourable mortgage loan.

What are the current mortgage rates?

In mid-2025, Swiss mortgage rates have stabilised after several months of volatility.

- The 10-year fixed rate averages between 2.1% and 2.6%

- The SARON rate (Swiss Average Rate Overnight) currently fluctuates around 1.5% to 2%, depending on the institution

- Mixed mortgages (fixed part + SARON part) remain an interesting intermediate option

Conditions vary from lender to lender, so it’s important to compare offers to find the most advantageous option.

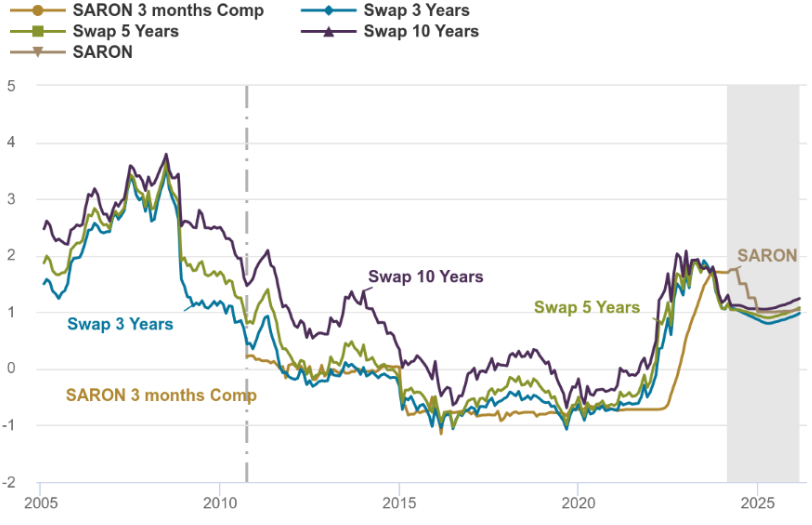

Rate evolution in % | Sources: Bloomberg, UBS Switzerland SA (This is an indicative interest rate. The effective interest rate is calculated from the margin and the Compounded SARON of the counting period. Compounded SARON cannot be negative.)

Here is how to interpret this chart:

SARON:

- Money market base → changes daily.

- If you take a SARON mortgage, you pay: SARON + bank margin (~0.8% to 1.5%).

SWAP:

- Allows a bank (or you indirectly) to lock this variable rate over a given period.

- Example: SARON swap → fixed rate for 5 years.

- The longer the duration, the more the swap rate includes a time risk premium.

Fixed rate currently offered by banks and insurers:

- Result of SARON + swap rate + bank margin.

- This is the rate you see on comparison websites.

What are the rate forecasts until the end of the year?

Analysts anticipate a slight easing of fixed rates by the end of 2025 if inflation continues to slow. However, the SNB remains cautious, and increases or decreases will depend on several factors:

- The evolution of the Swiss GDP and main economic indicators

- The stability of inflation, currently close to 2%

- Monetary policy decisions made by the European Central Bank (ECB) and the US Federal Reserve (Fed), which indirectly influence Switzerland

In the short term, a return to pre-2022 low rates should not be expected. Caution remains essential, especially for variable rate borrowers.

| Example Bank | 10-year fixed rate | Variable rate (SARON) |

|---|---|---|

| UBS | 1.43% – 1.48% | 0.96% + SARON |

| Credit Suisse | ~ 1.65% | Not specified |

| Raiffeisen | ~1.50% | ~ 1.50% |

Which factors influence mortgage rates?

Several elements determine the rates offered by banks and other financial institutions:

- SNB monetary policy: its key rate guides refinancing costs for banks

- Inflation: rising prices generally push rates up

- Overall economic conditions: growth, employment, geopolitical tensions…

- Risk level of the file: personal contribution, income, job stability, type of property financed

Each borrower therefore has a unique profile that will influence the conditions obtained. You are unique, and your file must reflect that. Your happiness in your home or apartment depends on it.

Fixed rate, variable rate, or mixed mortgage: how to choose?

Mortgage rates have a direct impact on your financial decisions: overall budget, purchasing power, choice between fixed rate or SARON… A variation of a few tenths of a point can represent several thousand francs in the long term. Also, regularly monitoring their evolution allows you to anticipate the best times to borrow or renegotiate your loan, and prepare for possible market fluctuations (especially if you opt for a variable rate or if your contract is about to expire).

The choice of rate type depends on your profile, risk tolerance, and wealth strategy.

| Mortgage type | Advantages | Disadvantages |

|---|---|---|

| Fixed rate | Security Stable monthly payments, Ideal for tight budgets | Less flexibility Rates often higher than SARON |

| SARON rate* | Lower initial rate Potential savings if rates fall | Revised every 3 months Risk of unexpected increase |

| Mixed mortgage | Combines stability and opportunity | More complex to manage |

*SARON is recalculated every business day and applied on average every 3 months. It is therefore more volatile but can be interesting if you anticipate a rate decrease in the medium term.

Feel free to contact one of our mortgage brokers for personalized advice and use our online simulator for a quick, free, and non-binding first personalized estimate.

Frequently asked questions about mortgage rates

How does rate fluctuation impact my mortgage loan?

A rate increase raises the overall cost of credit, especially for variable mortgages. A 2% rate instead of 1.5% on a loan of 800,000 CHF can represent several thousand francs extra over the term.

What is the current key interest rate?

Since July 2025, the key interest rate of the Swiss National Bank (SNB) has been set at 1.25%. This rate directly influences the cost of credit for banks and, consequently, the mortgage rates offered to individuals. The SNB adjusts its rate based on inflation, the economic situation, and the stability of the Swiss franc. It is therefore essential to monitor its evolution if you are considering a mortgage loan.

When is the right time to borrow?

The “right time” depends on your project. Rather than waiting for a hypothetical rate drop, it is better to secure an attractive offer as soon as you are ready to buy. Rates can move quickly.

Will mortgage rates increase?

It is difficult to answer with certainty, as mortgage rates depend on many factors: SNB monetary policy, inflation, economic situation, international rates, etc.

In summer 2025, the trend is rather stabilization, with slight fluctuations depending on the types of mortgages and institutions. However, a rise is not excluded if inflation goes up again or if the SNB adjusts its key interest rate once more.

Rather than speculating, it is better to compare current offers and lock in an attractive rate as soon as you are ready. Our brokers can help you anticipate wisely.

How to choose the right lending institution?

Each bank applies its own pricing grids. The best rate is not everything: repayment conditions, flexibility, support are also to be compared. A broker can help you play the competition.

What is the difference between the advertised rate and the personalized rate?

The advertised rate by banks is often indicative. The personalized rate depends on your profile (income, equity, type of property, financing ratio, etc.). It can be more advantageous if your file is solid. Hence the benefit of going through a broker to negotiate better.

Can a mortgage be renegotiated before maturity?

Yes, it is possible in some cases, especially near the end of the contract. You can also consider a refinancing with another bank. It is important to take into account any early exit penalties. A broker can help you make the right calculations.

Can the SARON rate exceed the fixed rate?

Yes, it is possible, especially during periods of rapid increases in key interest rates. SARON is indexed on short-term Swiss money market rates, so it can vary upwards. This represents a risk for borrowers seeking stability.

Can I change the type of rate during the contract?

It depends on the initial contract. Some mortgages offer a conversion option (for example, switching from a SARON rate to a fixed rate). But it is not systematic. You must check the terms of your contract or consult a broker before signing.